Understanding what succeeds provides insight into viable strategies:

Ultra-Prime Locations

Luxury and premium brands in flagship malls continue reporting strong performance. Industry sources indicate many luxury retailers experienced approximately 20% sales growth in 2024, driven by tourist spending and high-net-worth resident demand. These locations justify premium rents through exceptional foot traffic, international brand exposure, and affluent customer demographics.

Community-Focused Retail

Neighborhood malls serving growing residential areas demonstrate consistent occupancy success. These locations benefit from:

- Captive local demand: Residents seeking convenience for daily needs

- Lower rental costs: More sustainable economics for tenants

- Reduced competition: Serving defined geographic catchments

- Essential services focus: Supermarkets, pharmacies, services, and F&B

Dubai's population growth approximately 3.5% annually according to various estimates continues supporting well-located community retail.

Experience-Driven Categories

Food & beverage, entertainment, beauty services, and wellness concepts consistently outperform traditional retail. These categories offer experiences that e-commerce cannot replicate:

- Immediate gratification: Dining and entertainment are inherently physical

- Social experiences: Gatherings and activities that create memories

- Service components: Personalized attention and expertise

- Sensory engagement: Taste, atmosphere, and live interactions

Savvy mall operators increasingly allocate space toward these categories while reducing traditional retail footprints.

Strategic Considerations for Retailers and Investors

Based on current market dynamics, several strategic approaches merit consideration:

For Mid-Tier Apparel Retailers

1. Reconsider Secondary Super-Regional Locations

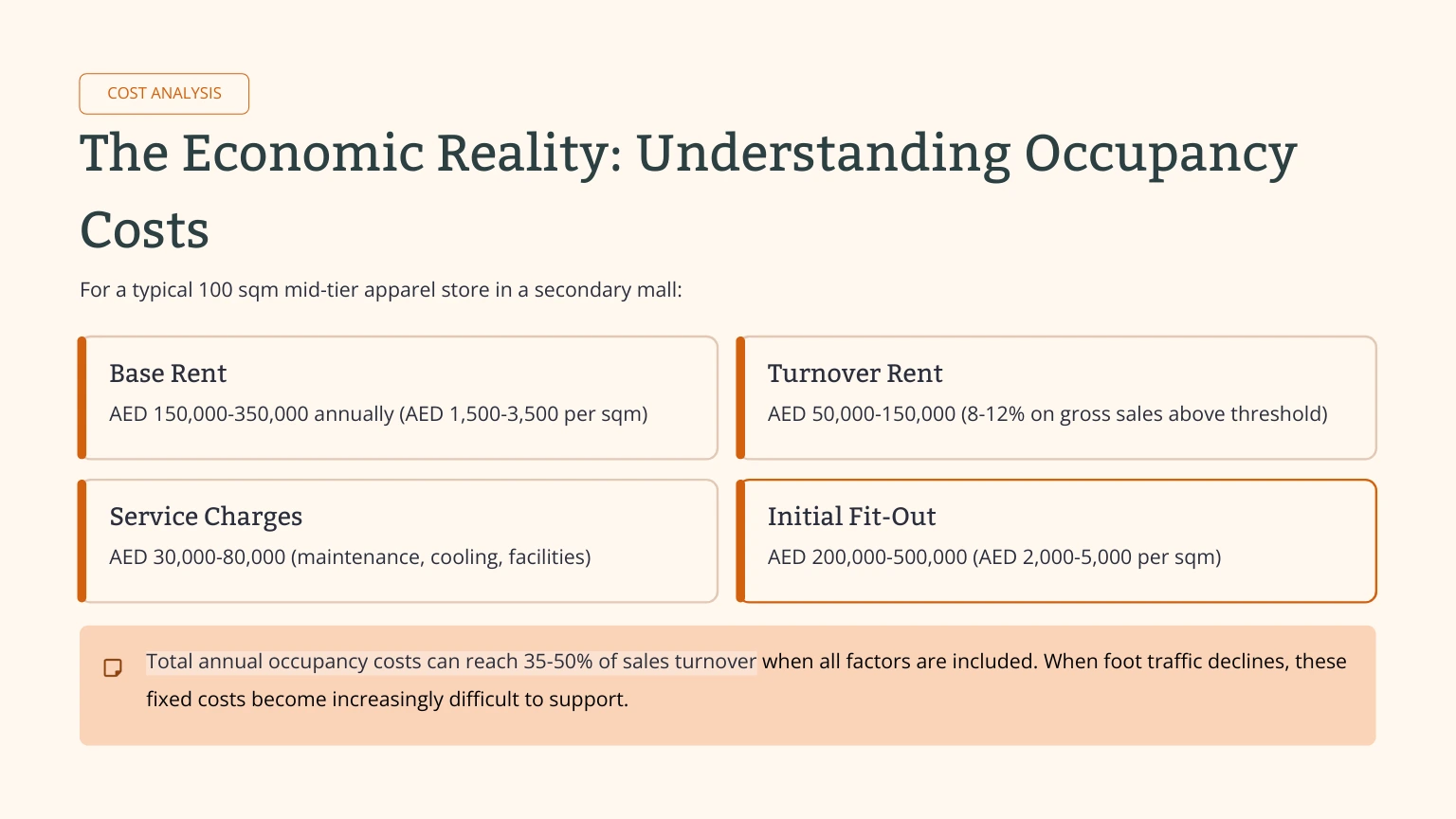

Unless negotiating exceptional terms extended rent-free periods (6-12 months), substantial fit-out contributions, flexible exit clauses, and below-market rental rates carefully evaluate whether secondary mall locations align with your business model. The structural headwinds may outweigh location benefits.

2. Embrace Omnichannel Integration

Physical retail must complement digital channels rather than compete with them. Consider:

- Treating stores as brand showrooms and experience centers

- Accepting that 40-60% of sales may occur online

- Reducing physical footprint to optimize economics

- Integrating inventory systems for click-and-collect

- Training staff to support digital journeys

3. Target Community Mall Opportunities

Growing residential areas with new community malls offer more favorable economics:

- Lower rental costs improve profitability thresholds

- Convenience-driven traffic is less discretionary

- Reduced competition from online alternatives

- Sustainable long-term demand from population growth

4. Create Differentiated In-Store Experiences

If operating in secondary malls, justify customer visits through unique experiences:

- Personal styling and consultation services

- Exclusive in-store product collections

- Events, workshops, and community engagement

- Complementary services (alterations, customization)

- Elevated customer service that online cannot match

For Real Estate Investors

1. Recognize Format Differentiation

Not all retail real estate performs equally. Success increasingly depends on clear positioning:

- Flagship destinations: Require scale, tourist appeal, and experiential elements

- Community convenience: Serve defined residential catchments efficiently

- Specialty/lifestyle centers: Offer unique positioning (outlet, luxury, thematic)

Generic secondary super-regional malls without clear differentiation face the most challenging outlook.

2. Tenant Mix Evolution

Forward-thinking mall operators are shifting tenant mix toward less e-commerce-vulnerable categories:

- Increasing F&B allocation from 15-20% to 25-35% of GLA

- Adding entertainment and leisure concepts

- Emphasizing services over goods retail

- Curating unique concepts unavailable elsewhere

3. Realistic Underwriting

When evaluating retail investments, particularly in secondary locations:

- Model realistic vacancy assumptions for vulnerable categories

- Stress-test against continued e-commerce growth

- Evaluate location convenience and catchment strength

- Assess differentiation versus competing centers

- Consider tenant rollover and leasing costs

Looking Ahead: The 2026-2027 Outlook

Several trends will likely shape Dubai's retail landscape in the near term:

Tourism Momentum Continues

Dubai's tourism sector maintains strong fundamentals. While specific numerical targets for 2026 vary across sources, continued growth in international visitor arrivals appears likely given infrastructure investments, event calendars, and global tourism recovery trends.

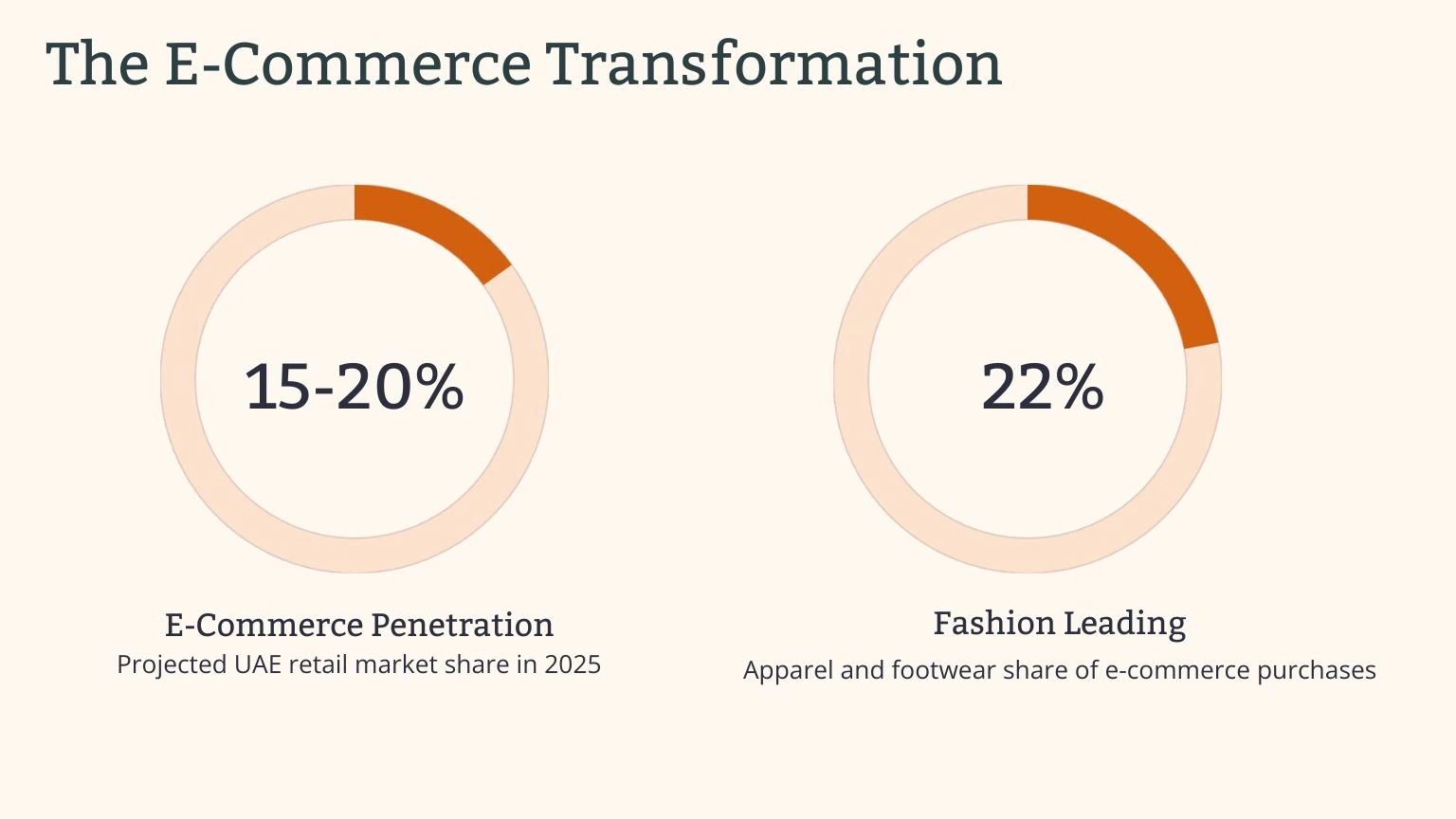

E-Commerce Maturation

Digital retail penetration will continue expanding, potentially reaching 15-20% of total retail sales by end-2025 or early 2026. Fashion and electronics will remain leading online categories, further pressuring traditional apparel retail models.

Market Consolidation Expected

The structural challenges facing mid-tier retailers in secondary locations suggest continued market adjustment. This may manifest as:

- Selective store closures in underperforming locations

- Lease renegotiations with more favorable tenant terms

- Increased turnover in vulnerable retail categories

- Landlords offering greater concessions to maintain occupancy

New Supply on the Horizon

Major projects like Dubai Square (2028+ opening) will add substantial new retail inventory to the market. While these flagship developments may succeed individually, they will increase competitive pressure on existing secondary properties.

Successful Adaptation Required

Retailers and landlords demonstrating adaptability will likely outperform:

- Retailers: Those integrating digital and physical seamlessly

- Landlords: Those curating differentiated, experience-focused tenant mixes

- Both: Those recognizing and responding to structural market changes

Conclusion: Navigating the New Retail Reality

Dubai's retail market in 2026 reflects broader global trends: the flight to quality, digital disruption, and experience-driven consumption. While aggregate statistics suggest market health, significant variation exists across segments and formats.

Mid-tier apparel retailers face genuine structural challenges in secondary mall locations, challenges unlikely to resolve through economic cycles alone. The combination of e-commerce convenience, market polarization, location disadvantages, and substantial occupancy costs creates difficult operating conditions.

Success in this environment requires honest assessment of these realities and strategic adaptation:

- Retailers must embrace omnichannel models, seek favorable locations, and create compelling reasons for physical visits

- Investors must differentiate between retail formats, recognize vulnerable segments, and underwrite conservatively

- Developers must curate distinctive, experience-focused destinations rather than generic retail collections

The future belongs to those who recognize that retail real estate is no longer primarily about providing space for transactions; it's about creating destinations, experiences, and communities that complement rather than compete with digital alternatives.

About Astra Terra Properties

Astra Terra Properties is a Dubai-based real estate advisory firm specializing in luxury residential and commercial property markets. Our commercial division provides institutional investors, retailers, and developers with data-driven insights and strategic advisory services across the GCC region.

This analysis represents our assessment of current market conditions based on publicly available information, industry research, and professional experience. It should not be considered financial advice or a substitute for professional consultation.

Sources and References

This analysis incorporates publicly available information from:

- Cushman & Wakefield - "Main Streets Across the World, 35th Edition" (2025)

- Various commercial real estate research reports on Dubai retail market (2024-2025)

- Mordor Intelligence - "UAE E-commerce Market Industry Report" (2024-2025)

- Digital Commerce 360 - UAE e-commerce market analysis

- Dubai Department of Economy and Tourism - Tourism statistics

- Industry publications and market reports from recognized commercial real estate firms

- Third-party retail intelligence platforms and market data providers

All statistics and data points represent estimates and projections based on available information as of January 2026. Market conditions are subject to change.

For inquiries regarding Dubai commercial real estate opportunities:

📧 commercial@astraterra.ae

📱 +971 58 558 0053

🌐 www.astraterra.ae

Frequently Asked Questions: Mid-Tier Retail in Dubai 2026

Q1: Are secondary malls in Dubai still profitable for retailers in 2026?

Yes, but selectively. Secondary malls anchored by strong community demographics — high residential density, limited competing retail, established foot traffic from gyms, supermarkets, and F&B — continue to perform well. Malls in JVC, Al Barsha, and Discovery Gardens maintain 85–92% occupancy rates (CBRE Retail Market Report Q4 2025). Malls that lack a compelling anchor tenant or community catchment are struggling with occupancy below 70%.

Q2: What are typical retail lease rates in Dubai's secondary malls?

Ground floor retail in secondary community malls typically ranges AED 150–350 per sqft annually, compared to AED 500–1,200+ per sqft in primary malls like Dubai Mall or Mall of the Emirates. Service charges add AED 30–80 per sqft depending on the mall's amenity level. For F&B units with kitchen extraction requirements, landlords increasingly demand fit-out contributions in lieu of rent-free periods.

Q3: How has e-commerce affected Dubai's secondary retail market?

E-commerce penetration in the UAE reached 15.3% of total retail sales in 2025 (Euromonitor International), with grocery and electronics most impacted. However, experiential categories — F&B, fitness, beauty services, and speciality retail — have proven e-commerce-resistant and are driving the strongest demand for secondary mall space. The shift is structural: commodity retail is migrating online while experience-led retail is capturing physical space.

Q4: What lease terms should commercial tenants negotiate in 2026?

In the current market, tenants have more leverage than they did in 2022-2023. Focus on: (1) A minimum 3-year initial term with 2-year renewal options at capped increases; (2) Turnover rent clauses on years 2-3 to share risk; (3) Fit-out periods of 60-90 days rent-free; (4) Break clauses at year 2 if sales targets are not met; (5) Right of first refusal on adjacent units. Landlords in secondary malls are increasingly willing to negotiate on all five points.

Q5: Is it better to buy or lease retail space in Dubai's secondary malls?

For established businesses with 5+ years of proven Dubai trading history, purchasing strata-titled retail units in secondary malls can offer a compelling AED cost structure — prices range AED 1,200–2,800 per sqft in community retail centres. Gross rental yields on purchased retail units range 7–10% in mid-tier locations. For new entrants testing a concept, leasing is lower risk. See our guide to retail business costs in Dubai for a full breakdown.

Sources & References

- CBRE Dubai Retail Market Report Q4 2025

- Knight Frank UAE Commercial Property Outlook 2026

- Dubai Land Department (DLD) — Commercial Transactions Data 2025

- Euromonitor International — UAE E-Commerce Penetration Report 2025

- JLL Dubai Retail Occupancy Survey Q3 2025

Joseph's Take: The Hidden Opportunity in Dubai's Secondary Retail Market

The narrative around secondary malls in Dubai is more nuanced than the headlines suggest. Yes, some malls are struggling. But I've watched community retail centres in JVC, Jumeirah, and Al Barsha maintain near-full occupancy through every market cycle, and those properties continue to attract serious commercial investors precisely because their tenant mix is built on necessity — pharmacies, medical clinics, supermarkets, F&B — not discretionary luxury.

The opportunity I'm seeing in 2026 is in mid-market F&B concepts targeting Dubai's expanding professional and family residential base. The communities being developed today — Expo City, Dubai South, and the JVC expansion — are creating demand for quality casual dining and speciality food that existing secondary malls are not yet serving well. First-mover advantage in these emerging catchments can be significant for the right operator.

For commercial property investors, I'd direct attention to community-anchored retail strips — not malls — in established residential communities like Mirdif, Jumeirah Village Triangle, and Remraam. Strip retail in these areas transacts at AED 1,000–1,800 per sqft with net yields of 8–10%, supported by captive residential demand that is genuinely sticky. If you're evaluating commercial investment opportunities in Dubai, speak with me at +971 58 558 0053 or astraterra.ae/contact